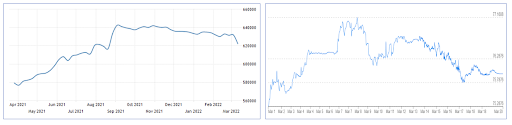

The last two weeks have seen a sharp decrease of $10billion in India’s forex reserves. In ordinary circumstances this would have raised alarm bells of investors pulling out dollar deposits in search of better returns from the long anticipated and now confirmed first of a series of 25 basis points rate hikes by Jeremy Powell.

Although this may well be true, the picture is incomplete without considering the impact of the Russia-Ukraine war on our coffers. With the reduced reserves the RBI has strengthened the rupee making our oil import bill more palatable to an already inflated fiscal deficit which was pegged to be at 6.8% but is currently hovering closer to 7%. This overshooting of the fiscal deficit should come as no surprise given FM Nirmala Sitharaman’s statement, during the budget, to nurture growth through continued public investments.

Figure 1: India Forex reserves in $ (left), Rupee Exchange rate (right)

Figure 1: India Forex reserves in $ (left), Rupee Exchange rate (right)

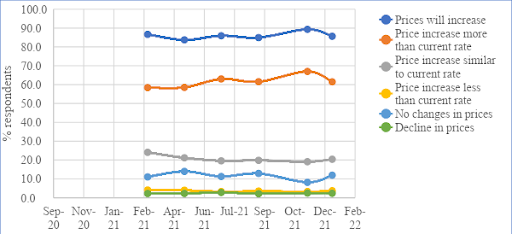

Will the RBI announce a retaliatory repo rate hike this April? The answer to this is twofold. Undoubtedly the inflation rate has been rising since October 2021. However, it is heartening to see it stay just within the less than 6% target RBI sets for itself – showing first signs of plateauing. This is supplemented by RBI inflationary expectation survey from February 2022 which shows a nearly 5% decrease in respondents expecting a raise in prices in both the 3 month and one year time horizon. So, it is unlikely the inflation rates have been cemented into new labour and loan contracts yet. All this points to a continued accommodative stance by the RBI in April – and it is unlikely to chase the Fed’s tail.

Figure 2: RBI inflationary expectations survey

Figure 2: RBI inflationary expectations survey

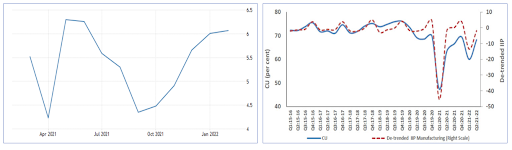

But is the RBI repo rate announcement the be all and end all? No, there is more to it than meets the eye. The government recently announced $3.3 billion green bonds will be up for sale. On the face of it the move is intended to shield the economy from the volatility of oil prices with investments in green tech, but purchase of these green bonds further sucks out liquidity in the market and may well be termed as a covert means to hike the repo rate without spooking the markets already uncertain about the Russian-Ukrainian war and an economy just about showing signs of recovery with capacity utilisation that was hovering closer to 60% for most of the last fiscal is now inching towards 70.

Figure 3: India Inflation rate(left) & Capacity utilisation (right)

Figure 3: India Inflation rate(left) & Capacity utilisation (right)

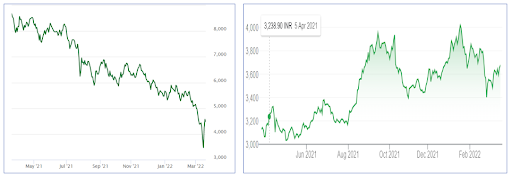

The strengthened rupee from the decreased reserves and green bonds sales will aid imports of most the green tech. How this sits in with the Atma Nirbhar vision is still unclear. For now, the message is buoyed by strong performance of the Indian tech stocks versus the Hang Seng Tech Index which has seen nearly 50% drop since the US started targeting Chinese tech a year back for their poor auditing standards. The Indian government is confident a strengthened rupee will not hurt tech exports and will, in fact, aid import of the much of the green tech needed to support the green bonds.

Figure 4: Hang Seng Tech Index (left) & TCS stocks (right)

Figure 4: Hang Seng Tech Index (left) & TCS stocks (right)

One however needs to watch this space carefully, for now Chinese investors, spooked by the possible sanctions on China as it seems to be showing signs of supporting Russian aggression, are pulling their tech investments into India. However, it would be fastidious to consider our Chinese counterparts to not respond to this with a more accommodative stance. The 25% jump in Alibaba’s stock following a prolonged slump, after last week’s meeting chaired by Chinese vice premier Liu He indicating a return to steps to ‘invigorate the economy’ is a case in point. Further, the supply side disruptions resulting from an extended Russian-Ukrainian war are still unclear. The impact of the remaining 5 US rate hikes is also yet to play out. For now, the RBI is carefully calibrating the triad of repo rate, exchange rate and capital flows to ensure the government doesn’t have to foot a huge oil bill and also meets its inflationary targets. The asymmetric nature of the shock to the US and Indian economy is playing to the RBIs advantage but some of the risks particularly if investors decide to flock back to Chinese tech stocks will truly test the RBI’s resolve.

Sources:

Hang Seng Index: https://www.hsi.com.hk/eng/indexes/all-indexes/hstech

Rupee exchange rate: https://www.xe.com/currencycharts/?from=USD&to=INR&view=1M

India inflation data: https://tradingeconomics.com/india/inflation-cpi

India capacity utilisation: https://rbi.org.in/Scripts/PublicationsView.aspx?id=21000

Inflationary Expectations: https://m.rbi.org.in//Scripts/BimonthlyPublications.aspx?head=Inflation%20Expectations%20Survey%20of%20Households%20-%20Bi-monthly

Ram Iyer is an alumni of EPGP 2021-22. He is an automotive SME with Latent View Analytics. In his spare time he enjoys long walks with his own good company, music and cars.